Economic theory postulates that, all other things being equal, investors should require a higher return in compensation for taking on more illiquid investments, the so-called ‘illiquidity premium’.

Property is one asset class where there are ‘liquid’ and illiquid investment structures and where we can test the theory.

I’ve deliberately placed the term liquid in quotation marks to highlight that, while there is daily trading of listed commercial real estate (CRE) vehicles, many of them are small- to mid-cap in size.

Unlike large liquid blue chips, listed REITs have limited true liquidity in that institutions cannot trade large blocks of REITs on the market without having a price impact. This is the first clue as to why the property illiquidity premium would not be as strong as theory suggests.

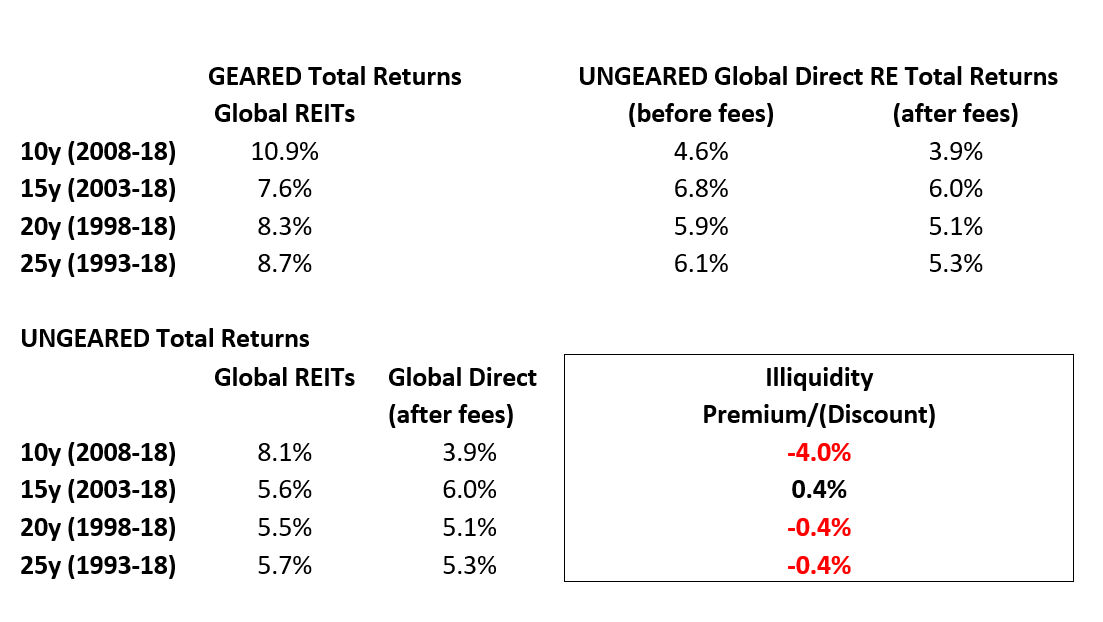

Atchison Consultants have a constructed time series of global direct property total returns starting in 1989. We can compare these against Global REIT total returns[1] to verify if the theory approximates reality.

With the exception of the 15-year period (2003-18), the data strongly suggests that for global property the so-called illiquidity premium remains elusive.

Portfolio managers of listed REITs tend to use this as an argument for investing in REITs as opposed to unlisted property. After all, why would rational investors want to invest in the illiquid version when they can access the ‘liquid’ version at no additional cost (in the form of lower returns) to its illiquid counterpart?

Rather than a purist either-unlisted-property-or-listed-REITs approach, it is more informative to acknowledge the facts on the ground and ask what institutions are implying by their investment decisions.

Institutions invest BOTH in unlisted property and listed REITs. There are at least a couple alternative hypotheses that may be inferred from this. These may more than offset the so-called illiquidity premium (if it did exist):

- Time diversification: Institutions attach value to the appraisal lag in unlisted property valuations

- Premium for Control: Unlisted property provides greater investor control in separate accounts, joint ventures and investment club situations than in fractional REIT ownership

Time diversification

Institutional allocation to unlisted property grew at the expense of REIT allocations as a result of the Global Financial Crisis (GFC) in 2008-09.

During the GFC, REIT returns imploded along with the broader equity markets, i.e. return correlations across most traded asset classes spiked to one. Moreover, investor horizons contracted from the long term to the immediate term.

In that scenario, any asset class (including unlisted property) that did not contract as fast as the general equity and debt markets was valuable as they moderated the asset price deflation in mixed asset portfolios. The appraisal lag in unlisted property valuations performed this role.

Despite taking a longer term approach to strategic asset allocations, the GFC experience showed that institutions do measure and value outcomes in shorter time horizons. In which case, institutions may have traded away some of that illiquidity premium for access to assets that lag listed assets in their valuation process.

(Price) Premium for Control

Most institutions take non-controlling (small), fractional ownership stakes in REITs to avoid:

- Ownership disclosure requirements (e.g. 5 per cent threshold)

- ‘Deemed control’ ownership thresholds in international jurisdictions for tax reasons

- Illiquidity of controlling stakes in small- to mid-cap shares

- Higher fees related to active management

Whereas, many institutional investors in unlisted property assert some form of positive[2] or negative[3] control.

We know from listed markets that investors are willing to pay a (price) premium for controlling stakes in publicly-traded firms. The same should hold true in property markets, public and private.

All other things being equal, a price premium for control means accepting a lower return. This lower return for control may (more than) offset any illiquidity premium for unlisted property.

Rohan Shan is an independent consultant, based in Brisbane. Until 2019, Rohan spearheaded QIC Global Real Estate’s top-down investment risk and strategy research function. He oversaw QIC’s domestic and international property portfolios for over 12 years.

[1] FTSE EPRA/NAREIT Global REITS Total Returns (Unhedged AUD)

[2] e.g. separate account, JV, club-style investments

[3] e.g. investor advisory board representation for pooled funds

__________

[i3] Insights is the official educational bulletin of the Investment Innovation Institute [i3]. It covers major trends and innovations in institutional investing, providing independent and thought-provoking content about pension funds, insurance companies and sovereign wealth funds across the globe.