Australia’s $2.2 trillion superannuation (pension fund) industry is facing a demographic tsunami as members approach retirement age. This ageing member base has a lower tolerance to risk in the portfolio, including loss of capital (loss aversion), volatility (risk aversion) and market downturns just before the member plans to retire (sequencing risk).

Institutional investors in other markets may also relate to the problem of how to manage reduced risk appetites (for example, defined benefit funds, philanthropic entities with distinct capital beneficiaries and sovereign entities with a public reputation to manage).

The traditional solution is to de-risk the portfolio as the members move closer to retirement; say, by replacing part of an equities (growth asset) allocation with a fixed income (defensive asset) allocation.

The problem – particularly in this low-yield environment – is that this greatly impairs the fund’s ability to continue to grow savings to fund a reasonable standard of living for its members in retirement. In other words, the member might well have a smoother journey – and feel safer – in the lead-up to retirement, but find upon retiring that the cost of this ‘safety’ is that they do not have enough savings to live on in retirement.

The constant performance drag from buying expensive protection also creates pressure on funds that are compared in peer performance surveys and risks the fiduciaries fatiguing of (terminating) the protection strategy at exactly the wrong time.

Any institutional investor simply forgoing income to achieve lower risk is not really solving the problem, but swapping one problem for another.

But the alternative to de-risking – staying fully invested in equities (to access the equity risk premium) and buying protection – is equally nasty. Buying protection typically means buying downside protection, tail-risk protection or volatility dampening with options or other derivatives.

Protection can very effectively target the type of risks the investor is concerned with, but it is very expensive. In fact, the cost of the protection creates a performance drag that can harm the portfolio just like physically de-risking, so the fund has still not solved the problem of how to ensure that, while managing risks, the member is still strongly growing savings for retirement.

The constant performance drag from buying expensive protection also creates pressure on funds that are compared in peer performance surveys and risks the fiduciaries fatiguing of (terminating) the protection strategy at exactly the wrong time.

Institutional investors trying to make a difficult choice between these two risk management strategies (de-risking versus buying protection) should recognise both are suboptimal. A better way to solve this investment predicament is to design an innovative third way that works well in both the de-risking and buying protection scenarios.

Specifically, consider both a partial physical de-risking – which is clearly the most direct way to remove some downside risk, volatility and other unwanted consequences of full equity exposure – and finding a replacement for the equity risk premium forgone. What replacement? The answer is right under our noses: smart funds should be selling the expensively priced protection that other institutional investors are buying.

This creates a new income source for the fund – regular income from a ‘volatility risk premium’ from the option selling – which helps to fill the return gap left by the partial physical de-risking. This turns the ‘buying expensive protection’ problem on its head – the expensive pricing becomes an asset to a fund that is now the seller, not the buyer, of this risk protection.

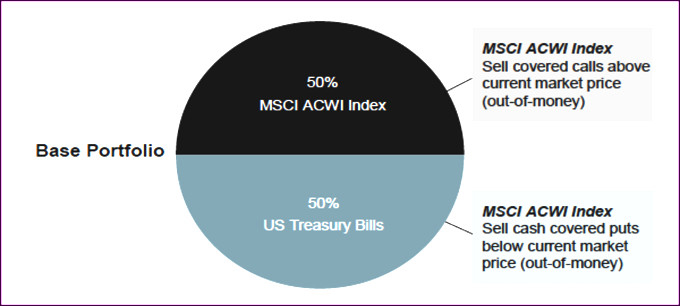

Practically, this creates a kind of ‘defensive equity’ portfolio that looks as follows:

Source: Parametric 2017

I have depicted a global equities portfolio here (spanning developed and emerging markets), 50 per cent de-risked into US Treasuries, but the concept works equally well in developed markets only (an MSCI World equity portfolio), the US (S&P 500) and Australia (S&P/ASX 200), and with most cash or short-dated fixed income assets.

It is an innovative way to address risks in an equity portfolio – playing ‘defence’ without the portfolio costs. Compared to a 100 per cent equities portfolio, the portfolio has around 40 per cent less volatility and downside and tail risks are confined to the 50 per cent physical equities portfolio plus just 50 per cent of the options overlay (not the full 100 per cent equities).

The structure depicted above is self-funded (fully collateralised), requires no leverage, uses listed instruments and is very transparent. The portfolio gives up some growth upside in very strong markets for less loss and a faster recovery in severe down markets, and produces a small, consistent outperformance over the equity market (from the premium income received) in all climates in between these extremes.

This idea shows the benefit of innovative thinking – if the choice is between two suboptimal alternatives, smart investors should reject the choice and design a much more optimal third way.

To access Parametric Australia’s full research papers, please visit: https://www.parametricportfolio.com/au/insights-research.

This information is for use with wholesale and qualified investors only and may not be distributed to the public. Not for use within the US, its territories or possessions, or with citizens or residents of the US.

For [i3] Insight’s guide to retirement, please click here.

__________

[i3] Insights is the official educational bulletin of the Investment Innovation Institute [i3]. It covers major trends and innovations in institutional investing, providing independent and thought-provoking content about pension funds, insurance companies and sovereign wealth funds across the globe.